Smart Ways to Invest In Bonds

Most investors are aware of the different types of stocks: big-company, small-company, technology, international and so on. And it may be a good idea to own a mix of these stocks as part of your overall investment portfolio. But the importance of diversification applies to bonds, too — so, how should you go about achieving it?

To begin with, individual bonds fall into three main types: municipal, corporate and government. Within these categories, you’ll find differences in the bonds being issued. For example, government bonds include conventional, fixed-rate Treasury bonds as well as inflation-protected ones, along with bonds issued by government agencies, such as the Federal National Mortgage Association (or Fannie Mae). Corporate bonds are differentiated from each other by several factors, but one important one is the interest rate they pay, which is largely determined by the credit quality of the issuer. (The higher the rating grade — AAA, AA and so on — the lower the interest rate; higher-rated bonds pose less risk to investors and therefore pay less interest.)

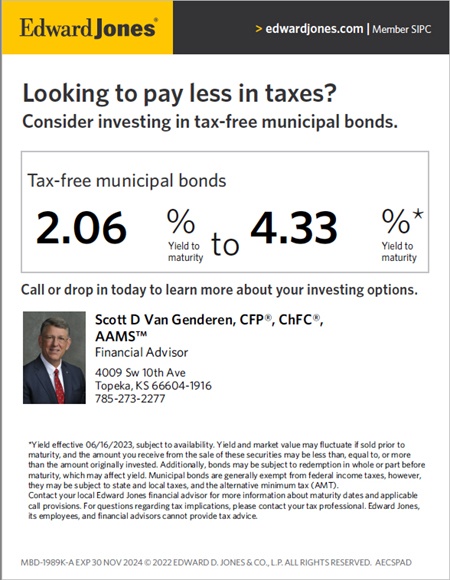

Municipal bonds, too, are far from uniform. These bonds are issued by state and local governments to build or improve infrastructure, such as airports, highways, hospitals and schools. Generally, municipal bonds are exempt from federal tax and often state and local taxes, too. However, because of this tax benefit, municipal bonds typically pay lower interest rates than many corporate bonds.

How can you use various types of bonds to build a diversified bond portfolio? One method is to invest in mutual funds that invest primarily in bonds. By owning a mix of corporate, government and municipal bond funds, you can gain exposure to much of the bond world. Be aware, though, that bond funds, like bonds themselves, vary widely in some respects. To illustrate: Some investors may choose a low-risk, low return approach by investing in a bond fund that only owns Treasury securities, while other investors might strive for higher returns — and accept greater risk — by investing in a higher-yield, but riskier bond fund.

But you can also diversify your bond holdings by owning a group of individual bonds with different maturities: short-, intermediate- and long-term. This type of diversification can help protect you against the effects of interest-rate movements, which are a driving force behind the value of your bonds — that is, the amount you could sell them for if you chose to sell them before they matured. When market interest rates rise, the price of your existing, lower-paying bonds will fall, and when rates drop, your bonds will be worth more.

But by building a “ladder” of bonds with varying maturities, you can take advantage of different interest-rate environments. When market rates are rising, you can reinvest your maturing, shorter-term bonds at the new, higher rates. And when market rates are low, you’ll still have your longer-term bonds working for you. (Generally, though not always, longer-term bonds pay higher rates than shorter-term ones.)

A bond ladder should be consistent with your investment objectives, risk tolerance and financial circumstances. But if it’s appropriate for your needs, it could be a valuable tool in diversifying your bond holdings. And while diversification — in either stocks or bonds — can’t always guarantee success or avoid losses, it remains a core principle of successful investing.

This article was written by Edward Jones for use by your local Edward Jones Financial Advisor. Edward Jones, Member SIPC

Scott D Van Genderen, CFP, ChFC, AAMS

Financial Advisor

4009 SW 10 Ave., Topeka, KS 66604-1916

785-273-2277

Scott.VanGenderen@edwardjones.com